Widgetized Section

Go to Admin » Appearance » Widgets » and move Gabfire Widget: Social into that MastheadOverlay zone

Colorado oil and gas drillers focused on cash flow, not increased production during energy crisis

For the second time in the past two weeks, a major Colorado oil producer told shareholders that it’s unlikely to ramp up production amid skyrocketing global energy prices, promising instead to funnel much of the additional cash flow into investors’ pockets.

Speaking on an earnings call Wednesday, Civitas Resources chairman and CEO Ben Dell told investors that the company’s financial decision-making this year will “come down to a discussion about what’s best, in terms of the easiest way to return capital” to Wall Street.

”We have a high base dividend, we’ve outlined our structure and calculation for the variable dividend — which, if commodity prices obviously are sustained, will continue to grow,” Dell said. “I think after that the real question is, how do you think about buybacks? How do you think about consolidation and infill (mergers and acquisitions)? And then, how do you think about a special dividend?”

Repeatedly throughout the call, Dell and other Civitas executives assured investors that its capital expenditures and reinvestment rates would remain low, even as oil prices surge above $100 a barrel for the first time in eight years.

“We’re very comfortable with our capital program for the year that we’ve already outlined,” Dell said in response to a question about raising the company’s number of drilling rigs in operation. “I don’t think you’ll see our strategy meaningfully divert from that.”

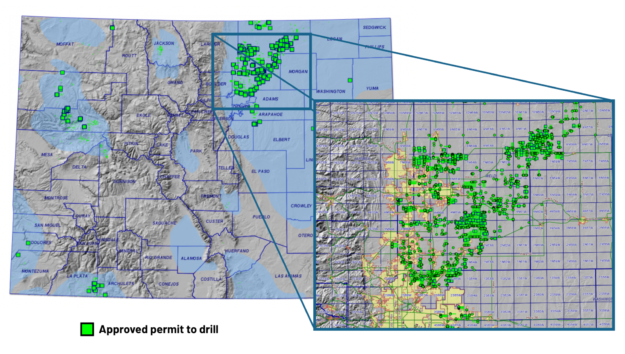

Civitas was formed last year as the result of a chain of mergers and acquisitions involving four of Colorado’s top nine oil producers: Extraction Oil and Gas, Crestone Peak Resources, Highpoint Operating and Bonanza Creek Energy. The new company just added a fifth sizable acquisition, privately held operator Bison Oil and Gas, in a deal announced last month. Combined, the five companies operate thousands of producing wells statewide — and have another 358 approved drilling permits in hand, according to data from the Colorado Oil and Gas Conservation Commission.

That stockpile is only a small portion of the nearly 3,000 approved permits to drill held by operators throughout Colorado, including roughly 1,900 in the oil-rich Denver-Julesburg Basin in the northeast quarter of the state. More than a thousand other wells have been reported to the COGCC by operators as currently being drilled, or already drilled but awaiting “completion” — the final stages of preparing a well for production, including hydraulic fracturing, or fracking.

But despite ongoing calls from Republicans at the state and national level for policymakers to “unleash” domestic oil production in response to Russia’s invasion of Ukraine, Civitas’ recent financial statements further underline the economic realities and investor demands that make a significant increase in drilling activity unlikely.

The dizzying consolidation that led to Civitas’ formation makes the new company a poster child for the wave of bankruptcies, acquisitions and mergers that have swept over the U.S. drilling industry in the last few years — both before and after the onset of the coronavirus pandemic.

The largest of Civitas’ predecessor firms, Extraction, acquired a notorious reputation among Colorado environmental activists for its envelope-pushing drilling projects near residential areas along the Front Range throughout the 2010s. It filed for Chapter 11 bankruptcy in June 2020 after years of concerns about its mounting debts.

The huge capital expenditures that Extraction and many other domestic drillers made during the “shale revolution” — referring to the shale oil reserves that could be tapped into thanks to technological advances like fracking and horizontal drilling — led to a dramatic boom in U.S. oil production in the 2010s, and in turn helped keep gas prices down. But Wall Street investors gradually soured on the industry in the latter half of the decade as debts piled up and many shale drilling projects proved less profitable than expected.

As a result, Wall Street has pressured the industry to show more “discipline,” and prioritize shareholder returns over reinvestment in new drilling projects. Under its new corporate brand, Civitas promised investors that it would “exemplify the new (exploration and production) business model for U.S. producers, with a focus on operational discipline, free cash flow generation (and) financial alignment with shareholders.”

In Colorado and beyond, industry trade groups and their GOP allies have used the global energy crisis to call for a variety of regulatory rollbacks and expedited approval processes that they say would help boost production. Colorado Rep. Lauren Boebert, a Republican from Silt, has urged the federal government to “immediately unleash our full energy potential,” and attended the State of the Union address earlier this month wearing a shawl emblazoned with the words “Drill Baby Drill.”

“Years of short-sighted policymaking at both the state and federal levels have contributed to where we are today,” said Lynn Granger, executive director of the American Petroleum Institute’s Colorado chapter, in a statement Thursday calling for additional COGCC permit approvals.

But in recent communications to shareholders, Colorado’s largest oil producers have consistently said much less about such regulatory concerns than about their financial fundamentals and commitments to limit production growth.

PDC Energy, Colorado’s third-largest oil producer, echoed Civitas’ message by outlining its “new return of capital framework” in an investor call last week. After its recent acquisition of Great Western Petroleum, the company holds more than 300 approved permits to drill, according to COGCC data; in an earnings statement, PDC said its stockpile of approved permits and drilled but uncompleted wells “represents an inventory life of more than ten years at the current development pace.”

Despite the continued dramatic rise in oil prices — a trend that shows no signs of slowing in the wake of President Joe Biden’s imposition of a Russian oil and gas import ban — few if any large U.S. oil drillers have given concrete indications that they plan to boost production. Scott Sheffield, CEO of Texas shale driller Pioneer Natural Resources, made headlines last month when he said his company wouldn’t change its growth plans even if oil prices reached $200 a barrel, though he later said he would reconsider if an unspecified “coordinated effort” to increase production took shape among Western governments.

The CEO of Colorado’s largest oil producer, Occidental Petroleum, was among the industry executives and analysts who downplayed the possibility of significant production growth at a conference this week. Oxy CEO Vicki Hollub told attendees at the annual CERAWeek energy summit in Houston that labor shortages and supply chain issues were among the contributing factors.

“If you did not plan for growth, you are not going to be able to achieve growth today,” Hollub said, according to Reuters. “Capital discipline today for oil companies is basically no (production) growth.”

That’s especially true for the fast-growing, free-spending drilling companies that once powered the shale revolution’s production boom in states like Colorado, Texas and North Dakota. Dell, founder and managing partner of the private equity firm Kimmeridge, which acquired Extraction in bankruptcy and brokered the mergers that formed Civitas, said Thursday that a more stable long-term outlook provides more certainty for investors.

“It’s clearly a highly cyclical and highly volatile industry,” Dell said. “The base assumption is that we’re going to stick to our existing plan and you’re not going to see a material shift in that, over the next 12 months to 24 months.”

Editor’s note: This story first appeared on Colorado Newsline, which is part of States Newsroom, a network of news bureaus supported by grants and a coalition of donors as a 501c(3) public charity. Colorado Newsline maintains editorial independence. Contact Editor Quentin Young for questions: info@coloradonewsline.com. Follow Colorado Newsline on Facebook and Twitter.

Chase Woodruff

Latest posts by Chase Woodruff (see all)

- Evans, Boebert defend Medicaid cuts as protesters shout them down in Denver - May 30, 2025

- Colorado officials envision Mountain Rail by 2026, Denver to Boulder to Fort Collins by 2029 - May 19, 2025

- Colorado’s Evans votes in favor of bill that will kick at least 7.6 million people off Medicaid coverage - May 15, 2025